The journey from “DeFi summer” in 2020 to today has been nothing short of wild. What started as a playground for early crypto nerds has grown into a serious financial infrastructure, with over $123.6 billion locked across protocols in 2025. But here’s the problem: if you’re new to DeFi, the sheer number of protocols can feel overwhelming. Aave? Compound? Curve? GMX? Where do you even start?

This guide cuts through the noise. Instead of throwing 50 protocols at you, we’re focusing on five core DeFi applications worth trying today. Each represents a different category—lending, swapping, yield farming, staking, and derivatives—so you get a complete picture of what DeFi can do. These aren’t random picks. They’re battle-tested protocols with solid track records, deep liquidity, and (relatively) beginner-friendly interfaces.

Think of this as your practical roadmap. We’ll explain what each protocol does, why it matters, what risks exist, and how you can start using it safely with small amounts. No hype. No promises of overnight riches. Just real tools that actually work.

What Is DeFi (In One Minute)?

Decentralized Finance—DeFi for short—is a parallel financial system built on blockchain technology, primarily Ethereum. Instead of banks and brokers controlling your money, smart contracts (self-executing code) handle everything automatically. You connect your crypto wallet directly to these protocols, keep control of your private keys, and interact with financial services without asking permission from anyone.

Here’s a simple example: Want to lend money and earn interest? In traditional finance, you deposit in a bank, they lend it out, and you get maybe 0.5% APY. In DeFi, you deposit crypto into a lending pool like Aave, borrowers take loans directly from that pool, and you earn 3-8% APY (or more, depending on market conditions). No middleman taking a cut. No credit checks. Just code executing automatically.

The trade-off? You’re responsible for your own security. No customer service to call if you send funds to the wrong address. No FDIC insurance if a protocol gets hacked. This is why starting small and learning the ropes matters so much.

How We Chose These 5 DeFi Apps

We didn’t pick these protocols randomly. Here’s what we looked for:

- Security track record: All five have been live for years without major hacks. They’ve survived multiple market crashes and have handled billions in transactions.

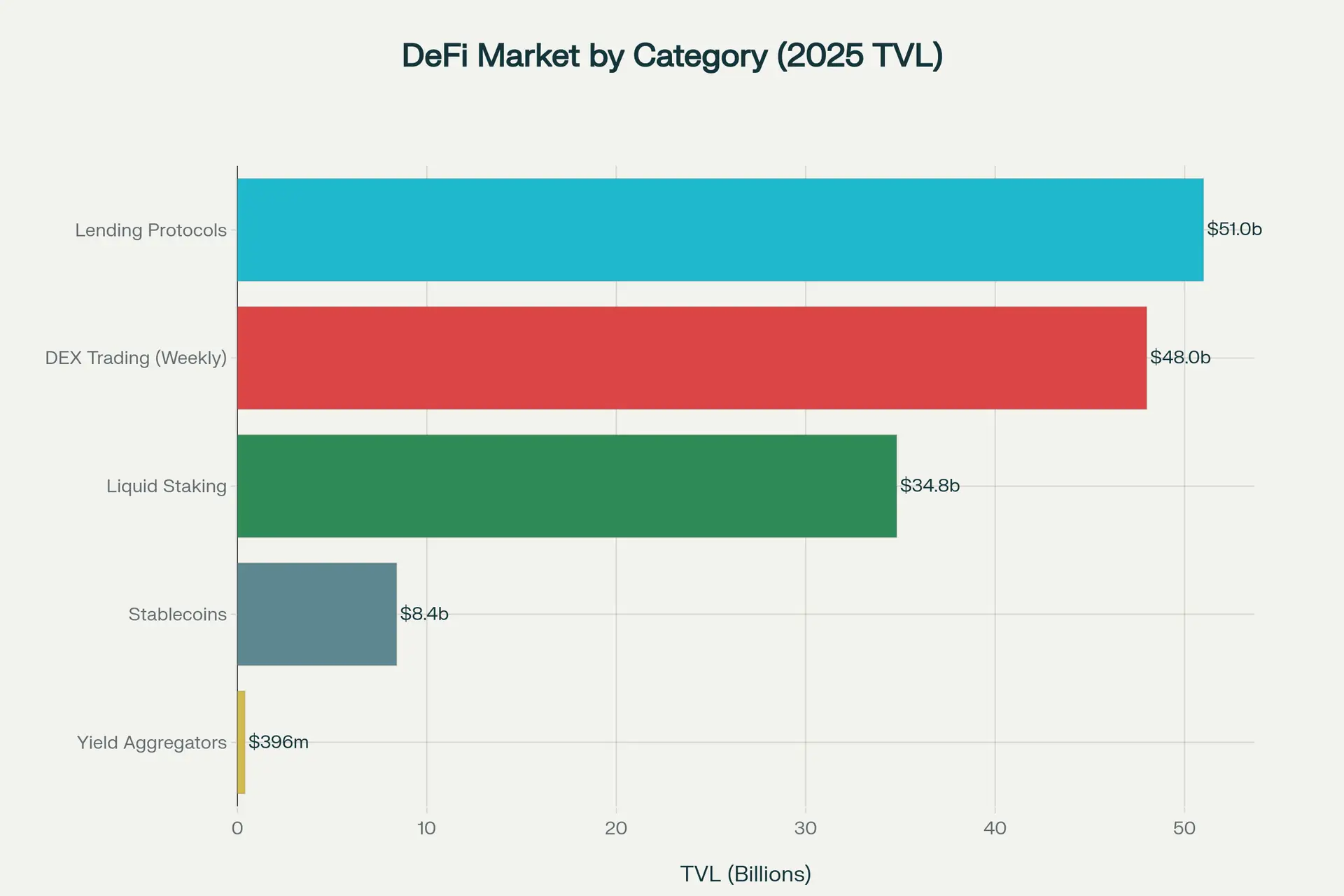

- Total Value Locked (TVL): Higher TVL generally means more trust from the market. Aave alone manages $36.98 billion, while Lido controls $34.8 billion in staked ETH.

- Longevity and battle-testing: These protocols launched between 2018-2020 and have been stress-tested through bull markets, bear markets, and everything in between.

- User experience: While no DeFi protocol is “easy” compared to Coinbase, these five have relatively clean interfaces and solid documentation.

- Beginner accessibility: You don’t need to be a Solidity developer to use them. Basic wallet setup plus some testnet practice gets you started.

That said, let’s be crystal clear: nothing in DeFi is risk-free. Smart contract bugs can drain funds. Market crashes can trigger liquidations. Phishing sites can steal your private keys. The protocols we’re covering have strong security, but risk never drops to zero.

#1 – Aave (Lending & Borrowing)

Category: Decentralized Lending Protocol

What it does: Lets you earn interest by supplying crypto, or borrow against your assets

TVL: $36.98 billion (2025)

Total active loans: $15.21 billion

Aave is the blue-chip lending protocol of DeFi. It’s non-custodial (you control your funds), supports multiple blockchains (Ethereum, Arbitrum, Optimism, Base, etc.), and offers both variable and stable interest rates. Think of it as a decentralized version of a savings account plus credit line—except way more flexible.

Here’s how it works in practice. Say you deposit 1,000 USDC into Aave. That USDC goes into a shared liquidity pool. Borrowers can take loans from that pool, and they pay interest. You earn a share of that interest automatically. Your balance grows in real-time. If the pool is earning 4.5% APY, you’ll see your aToken balance (the receipt token you get when you deposit) slowly increase.

On the borrowing side, you can use your deposited assets as collateral to borrow other tokens. For example, deposit $1,500 worth of ETH, borrow $1,000 worth of USDC (assuming 75% loan-to-value ratio). You still own the ETH—it’s just locked as collateral. As long as your collateral value stays above the liquidation threshold, your position is safe.

Aave V3 (the current version) introduced some powerful features:

- Efficiency Mode (E-Mode): Lets you borrow more when using correlated assets (like borrowing USDT against USDC)

- Portal functionality: Move liquidity across different blockchains seamlessly

- Umbrella Safety Module: Insurance fund that covers bad debt and protects the protocol

Pros:

- Industry-leading security (nine independent audits, massive bug bounty)

- Massive liquidity across 10+ networks

- Both variable and stable rate options for borrowers

- Proven track record since 2017

Risks:

- Liquidation risk: If your collateral drops below the required ratio, your position gets liquidated automatically and you pay a penalty (typically 5-10%)

- Collateral volatility: Using volatile assets like ETH as collateral means your ratio can swing wildly in crashes

- Smart contract risk: Bugs in the code could theoretically be exploited, though Aave’s security is top-tier

How to try it in 3 steps:

- Set up a wallet (MetaMask, Coinbase Wallet, etc.) and fund it with some crypto plus ETH for gas fees

- Go to app.aave.com, connect your wallet, choose which network you want to use (Ethereum, Arbitrum, Base, etc.)

- Deposit a small amount (like $50-100 worth of USDC or ETH) and watch interest accrue. Track your position daily to understand how rates fluctuate

Start with just supplying (lending) before you try borrowing. Get comfortable with the interface, watch how interest rates change, and understand the health factor before putting collateral at risk.

#2 – Uniswap (Decentralized Exchange)

Category: Decentralized Exchange (DEX)

What it does: Swap tokens peer-to-peer without a centralized orderbook

Trading volume: $85+ million daily (across all versions)

TVL: Part of the $48 billion weekly DEX volume

If you’ve ever rage-quit a centralized exchange because of withdrawal delays or frozen accounts, Uniswap will feel strangely liberating. It’s a fully decentralized exchange where you swap tokens directly from your wallet—no sign-up, no KYC, no asking permission.

Uniswap pioneered the Automated Market Maker (AMM) model. Instead of matching buy and sell orders like a traditional exchange, Uniswap uses liquidity pools. Here’s the simple version: liquidity providers deposit equal values of two tokens (say ETH and USDC) into a pool. When you want to swap ETH for USDC, you’re trading against that pool. A mathematical formula (x * y = k) sets the price automatically based on supply and demand.

Uniswap V4 launched in January 2025 with major upgrades:

- Hooks: Modular plugins that let developers customize pool behavior (dynamic fees, limit orders, custom oracles)

- Singleton architecture: All pools run through one smart contract, reducing gas costs by up to 99.99% for pool creation

- Flash Accounting: Only settles net balances at the end of transactions, making multi-hop swaps way cheaper

Here’s a real use case: You hold ETH and want to buy a smaller altcoin that’s not listed on Coinbase. Connect your wallet to Uniswap, select ETH as your input token, search for the altcoin you want, enter the amount, and confirm the swap. The transaction executes in seconds (depending on network congestion), and the new token appears in your wallet.

Pros:

- Deep liquidity for major pairs (ETH/USDC, WBTC/ETH, etc.)

- No account needed—just connect wallet and trade

- Access to long-tail tokens that’ll never get listed on centralized exchanges

- Permissionless: anyone can create a trading pair

Risks:

- Fake tokens: Scammers create tokens with identical names to real projects. Always verify contract addresses

- Slippage: On smaller pairs with low liquidity, your execution price can differ significantly from the quoted price

- MEV (Maximal Extractable Value): Bots can front-run your transactions, especially on large trades

- High fees on Ethereum: Gas costs can be $20-50+ during network congestion, though Layer 2s like Arbitrum and Base are much cheaper

Quick first-swap walkthrough:

- Practice on testnet first: Use Uniswap on a test network (like Sepolia) to understand the interface without risking real money

- Get a small amount of ETH: You need ETH both as the token to swap AND to pay gas fees

- Go to app.uniswap.org, connect your wallet, select tokens, enter amount, review fees and slippage tolerance (default is usually 0.5%), then confirm

- Check the transaction on a block explorer (Etherscan for Ethereum) to see the final execution price

Pro tip: For your first swap, stick to major pairs like ETH to USDC. Avoid obscure tokens until you understand how to verify contract addresses and check liquidity.

#3 – Yearn Finance (Yield Aggregator)

Category: Yield Aggregator

What it does: Automatically moves your funds between DeFi strategies to maximize returns

TVL: $396 million (2025)

Supported chains: Ethereum, Optimism, Arbitrum, Base, Polygon

Here’s the problem Yearn solves: chasing yields manually across DeFi is exhausting. One week, lending USDC on Aave pays 5%. Next week, Compound is offering 7%. Then a new liquidity mining program launches on Curve offering 12%. By the time you move your funds, the opportunity is gone.

Yearn Finance automates this grind. You deposit stablecoins (or other assets) into a Vault—think of it like a smart investment fund. Yearn’s strategies then deploy your capital across multiple DeFi protocols, automatically shifting between lending platforms, liquidity pools, and farming opportunities to capture the best available yields. You earn the boosted APY without touching anything.

For example, the USDC Vault might simultaneously:

- Lend some USDC on Aave to earn base lending yield

- Supply USDC to Curve stablecoin pools for trading fees

- Farm additional incentive tokens and auto-compound them back into USDC

All of this happens automatically. The Vault rebalances strategies when market conditions change. You don’t need to monitor gas fees, approve 15 different transactions, or time your moves.

Yearn v3 (launched late 2023) brought major improvements:

- Multi-strategy vaults: Single vault can run multiple strategies simultaneously, spreading risk

- Permissionless strategy deployment: More developers can build and test strategies, increasing innovation

- Optimized fees: Protocol-level fee reductions approved by governance

Pros:

- Set-it-and-forget-it automation—no manual yield chasing

- Strategies designed by experienced DeFi developers and audited

- Gas costs amortized across all vault participants (more efficient than doing it solo)

- Historical proven yields (though past performance doesn’t guarantee future results)

Risks:

- Strategy risk: Vaults can use complex, multi-layered strategies. If one underlying protocol fails, the entire vault can suffer

- Smart contract stacking: Your funds interact with multiple protocols. More complexity = more potential failure points

- Lower TVL than peak: Yearn’s TVL dropped from ~$5 billion peak to ~$400 million, reflecting broader DeFi consolidation

- Yield variability: APYs fluctuate significantly. A vault showing 15% might drop to 3% if market conditions change

Who it’s best for: People who want DeFi yields but don’t have time to actively manage positions across protocols. If you’re checking Aave rates vs Compound rates vs Curve pools every day, Yearn automates that grind.

How to use it:

- Go to yearn.fi, connect your wallet

- Browse vaults, look at historical APYs (shown on vault cards), read the strategy description

- Deposit a small amount, track performance over a few weeks

Start with a stablecoin vault (USDC, DAI, USDT) to minimize price volatility risk while you learn how the system works.

#4 – Lido (Liquid Staking)

Category: Liquid Staking Protocol

What it does: Stake ETH to earn staking rewards while keeping your assets liquid

TVL: $34.8 billion (2025)

Market share: 24.7% of all staked Ethereum

Ethereum staking is straightforward: lock up 32 ETH to run a validator, earn ~3-4% APY in staking rewards. The problem? Most people don’t have 32 ETH (~$76,000 at $2,400/ETH), and even if they do, locking assets for months isn’t appealing. You can’t trade your staked ETH, use it as collateral, or farm with it.

Lido fixes both problems. Stake any amount of ETH (even 0.01 ETH), and receive stETH (staked ETH) in return. Your stETH balance grows over time as it accumulates staking rewards. But here’s the key: stETH is a tradable token. You can sell it, use it as collateral on Aave, provide liquidity on Curve, or farm it elsewhere.

This is called liquid staking, and it’s become massive—representing 27% of total DeFi TVL by some measures. Why? Because it unlocks “double-dipping” strategies. You earn staking yield (~3%) from Ethereum validators, PLUS you can deploy stETH in other DeFi protocols to earn additional yield.

Real example:

- Deposit 10 ETH into Lido → receive 10 stETH

- Earn ~3% APY from Ethereum staking (stETH balance slowly grows)

- Deposit that stETH into Aave as collateral, borrow stablecoins, farm with those stablecoins

- Now you’re earning staking rewards + farming rewards simultaneously

Pros:

- Stake any amount—no 32 ETH minimum

- Keep liquidity: stETH can be used across DeFi (collateral, LP pairs, etc.)

- Deep liquidity: Lido is the largest liquid staking provider, stETH is widely integrated

- Competitive rewards: Same base ETH staking yield, plus composability opportunities

Risks:

- Depeg risk: stETH should trade 1:1 with ETH, but during extreme market stress it can trade at a discount (like the 5-8% depeg during the Terra collapse in 2022)

- Smart contract risk: Lido contracts hold billions, making them attractive targets for exploits

- Validator centralization concerns: Critics argue Lido’s dominance (24.7% of staked ETH) poses risks to Ethereum’s decentralization

- Slashing risk: If Lido’s validators misbehave (extremely rare), staked ETH can be slashed (penalized)

How to try it:

- Go to lido.fi, connect your wallet

- Enter amount of ETH you want to stake, confirm transaction

- Receive stETH in your wallet (appears automatically, balance increases daily)

- Optional: use stETH in other DeFi protocols or just hold it to accumulate staking rewards

If you’re holding ETH long-term and not actively trading it, liquid staking via Lido is a low-effort way to earn extra yield. The risk/reward is favorable for most holders.

#5 – GMX (Perpetual DEX)

Category: Decentralized Derivatives Exchange

What it does: Trade perpetual futures (up to 50x leverage) without a centralized orderbook

Monthly volume: $4.1 billion (GMX v2, October 2025)

Chains: Arbitrum, Avalanche

Most DeFi focuses on spot trading (swapping tokens you own) or simple lending. GMX opens up leverage trading—betting on whether crypto prices go up or down using borrowed funds. It’s the DeFi equivalent of futures trading on exchanges like Binance or Bybit, but fully on-chain and non-custodial.

Here’s how it’s different from other DEXs: Instead of an orderbook or AMM pools, GMX uses oracle-based pricing. You trade directly against a multi-asset liquidity pool (called GLP). When you open a long or short position, the pool takes the opposite side of your trade. Prices come from Chainlink oracles that aggregate data from major CEXs, so you get zero slippage (up to maximum open interest limits).

Real example: You think ETH will pump. Open a long position with 1 ETH and 10x leverage. If ETH goes up 5%, your position gains 50% (10x multiplier). If ETH drops 10%, you’re liquidated and lose your collateral. GMX supports up to 50x leverage, though beginners should start far more conservatively (2-5x max).

GMX v2 (current version) improvements:

- Enhanced capital efficiency through optimized liquidity pools

- Better price execution with multiple oracle sources

- Lower fees for frequent traders

Pros:

- Trade directly from your wallet—no account, no KYC

- Zero price impact (oracle pricing) for trades within open interest limits

- Multiple assets supported: ETH, BTC, AVAX, UNI, LINK

- Leveraged exposure without centralized exchange counterparty risk

Risks:

- Liquidation risk is extreme: With leverage, small price moves can wipe out your position. A 2% move against you with 50x leverage = liquidation

- Funding rates: Long or short positions pay (or receive) funding fees based on market imbalance. These compound hourly

- Oracle risk: If oracle price feeds are delayed or manipulated, traders can get bad execution

- Complexity: Leverage trading is hard. Most traders lose money, even experienced ones

Conservative beginner interaction:

If you must try GMX, here’s the safest approach:

- Start with tiny position sizes (like $20-50 max)

- Use low leverage (2-3x, not 50x)

- Set stop-losses to limit downside

- Close positions quickly—don’t let them run for days accruing funding fees

Honestly? Most DeFi beginners should skip derivatives entirely and stick to spot trading, lending, and staking. Perpetual futures are advanced tools that can destroy your capital fast. If you’re curious, paper trade first or use testnet versions.

Alternative option: MakerDAO (Stablecoin Protocol)

Since leverage trading isn’t for everyone, here’s a safer alternative in the 5th slot: MakerDAO, the protocol behind DAI stablecoin.

MakerDAO lets you generate the DAI stablecoin by locking crypto as collateral (similar to Aave, but you’re minting stablecoins instead of borrowing them). Lock $150 worth of ETH, mint 100 DAI. The DAI is pegged to $1, giving you stable purchasing power while maintaining upside exposure to your ETH collateral.

You can also earn 4.5% APY (as of 2025) by depositing DAI into the Dai Savings Rate (DSR). This is simpler than yield farming—just deposit DAI, earn interest automatically.

Why use DAI/MakerDAO?

- Generate stablecoins without selling your ETH (maintain long-term position while accessing liquidity)

- Decentralized stablecoin (more censorship-resistant than USDC/USDT)

- Earn passive yield on DAI holdings through DSR

Risks:

- Same liquidation risks as Aave if collateral drops

- Stability fee (interest rate) on minted DAI

- Governance changes can affect DSR and other parameters

MakerDAO is better for beginners than GMX. If you want to understand collateralized positions without leverage risk, start here.

How to Get Started Safely With DeFi

Here’s your practical checklist before touching real money:

1. Use a fresh wallet with small amounts

Don’t connect your life savings wallet to random DeFi protocols. Create a new MetaMask wallet, send $50-200 for testing. If something goes wrong, you lose $50, not $50,000.

2. Master wallet security basics

- Write down your seed phrase on paper (not digital). Store it securely

- Never share seed phrase or private keys with anyone

- Double-check URLs—phishing sites like “app.aavee.com” (extra ‘e’) steal funds

3. Always confirm correct URLs and contract addresses

Bookmark official sites (app.aave.com, app.uniswap.org, yearn.fi, lido.fi). Check contract addresses on official docs before interacting with tokens.

4. Check fees before confirming transactions

Ethereum gas fees spike to $50-100 during congestion. Use Layer 2s (Arbitrum, Optimism, Base) for 90% lower fees. Preview transaction costs in your wallet before confirming.

5. Set slippage tolerance carefully

Default 0.5% slippage is fine for major pairs. Increase to 1-3% for smaller tokens, but never above 10% (scam bots target high slippage).

6. Never ape into unknown contracts or copy random Twitter threads blindly

“100% APY stablecoin farm” threads are usually scams. Stick to established protocols with years of track record. If it sounds too good to be true, it’s a rug pull.

7. Track your positions actively at first

Check daily for the first week to understand how interest rates, liquidation ratios, and gas costs work. DeFi moves fast—positions that looked safe can approach liquidation during sudden crashes.

8. Start with stablecoins to reduce volatility risk

Your first positions should be stablecoin-focused (lend USDC on Aave, deposit DAI in Yearn). This isolates smart contract risk from market volatility risk.

Pros & Cons of Using DeFi vs Centralized Exchanges

DeFi Advantages:

- Self-custody: You control private keys and funds. No exchange can freeze your account or block withdrawals

- Permissionless access: No KYC, no approval process. Connect wallet and start trading immediately (assuming you have crypto)

- Financial sovereignty: Build positions, earn yields, and trade 24/7 without asking permission

- More innovation: New protocols ship features (liquid staking, flash loans, concentrated liquidity) years before CEXs copy them

- Access to long-tail assets: Thousands of tokens available that’ll never list on Coinbase

DeFi Disadvantages:

- Complexity: Managing wallets, gas fees, slippage, liquidation ratios requires learning

- Responsibility burden: No customer support. Mistakes (sending to wrong address, approving malicious contract) are irreversible

- Higher security risk on user: You’re responsible for wallet security. Phishing attacks and scams are common

- Gas fees: Ethereum transactions cost $5-50 during congestion (though Layer 2s solve this)

- Smart contract risk: Bugs can drain protocols. Even audited code isn’t 100% safe

Centralized Exchange Advantages:

- Ease of use: Simple interfaces, customer support, fiat on/off ramps

- Lower trading fees: Spot trading on CEXs often cheaper than DEX + gas

- Higher liquidity for major pairs: Tighter spreads on BTC, ETH, major altcoins

- Reversibility (sometimes): If your account gets hacked, exchanges might freeze funds and help recover

Centralized Exchange Disadvantages:

- Custody risk: Exchange holds your keys. FTX collapse proved this risk is real

- Withdrawal limits and restrictions: Exchanges can freeze accounts, delay withdrawals, or restrict access during volatility

- KYC requirements: Privacy trade-off for convenience

- Censorship risk: Exchanges must comply with regulations, potentially freezing assets

Final Thoughts – Which DeFi App Should You Try First?

Let’s recap the five protocols:

- Aave: Lending/borrowing, great for earning passive yield on stablecoins or ETH

- Uniswap: Token swaps, essential for accessing tokens not on CEXs

- Yearn Finance: Automated yield farming, good for set-it-and-forget-it strategies

- Lido: Liquid staking, perfect for ETH holders who want staking rewards + liquidity

- GMX: Leveraged perpetual trading (high risk, advanced users only) OR MakerDAO for stablecoin generation

Suggested order for beginners:

- Start with Uniswap (make a small swap on Arbitrum or Base to understand wallet connections and gas fees). This teaches you the basics without putting funds at risk for extended periods.

- Then try Aave (deposit stablecoins to earn interest). Learn how lending protocols work, track your interest accrual, understand health factors and liquidation risks.

- If comfortable, add Lido (stake ETH if you’re planning to hold long-term). This is low-maintenance and adds staking yield to a buy-and-hold strategy.

- Advanced users: Explore Yearn for automated farming strategies or GMX for leverage (with extreme caution).

The pattern is clear: start simple, understand one category before moving to the next, and always use small amounts while learning. DeFi rewards slow, deliberate experimentation. Rush in with large capital, and you’ll likely get wrecked by liquidations, scams, or smart contract exploits.

If you’ve ever rage-quit a CEX because of withdrawal issues, DeFi will feel strangely liberating. But that freedom comes with responsibility. Take your time. Learn the tools. And never invest more than you can afford to lose while you’re figuring things out.

Discover more from aiCryptoBrief.Com

Subscribe to get the latest posts sent to your email.

")