In August 2024, a trader on Reddit shared a painful story: they activated a futures grid bot with $1,000, did zero testing, and watched the account get liquidated overnight when Bitcoin wicked violently to $52,000. The bot kept buying into the move, stacking leveraged positions until there was nothing left.

Stories like this are disturbingly common.

Most beginners ask: “Which bot is best?”

Professionals ask: “How was this strategy tested, and how did it behave in bad markets?”

Over the first four days of this series on aicryptobrief.com, you’ve already seen:

- What AI crypto trading bots are and how they work (Day 1 & 2)

- How grid and DCA bots behave in different market regimes (Day 3)

- The most common mistakes people make with AI bots (Day 4)

This article provides the missing piece: a practical, step-by-step workflow for backtesting and paper trading your strategy before you risk a single dollar.

By the end, you’ll have a concrete testing plan that:

- Filters out weak or overfitted strategies early

- Sets realistic expectations for live performance

- Builds confidence to deploy small, controlled real capital

Disclaimer: This article is for educational purposes only and is not financial advice. Crypto and leveraged trading are highly risky. Always do your own research and never trade money you cannot afford to lose.

Backtesting 101: What It Is (and What It Is Not)

At its core, backtesting means replaying your trading rules on historical market data to see how they would have performed.

You define:

- Entry rules – when the bot opens a position

- Exit rules – when it closes the position

- Position sizing – how much to risk each trade

- Risk controls – stop-loss, take-profit, max drawdown limits

Then you run those rules over weeks, months, or years of past price data.

The output is a set of metrics:

- Total profit and loss (PnL)

- Maximum drawdown

- Win rate

- Average win vs average loss (risk–reward)

- Number of trades, and sometimes Sharpe ratio or other risk-adjusted metrics

Platforms like TradingView, 3Commas, Cryptohopper, and open-source tools like Freqtrade and Backtrader all provide backtesting engines tailored to crypto.

But backtesting is not a crystal ball:

- Markets change – volatility, liquidity, and correlations evolve

- What worked in 2021 or 2022 can fail in 2025

- Data quality, fees, and slippage assumptions can skew results

The real purpose of backtesting is simple:

Kill bad strategies cheaply, before they kill your capital.

Crypto makes this harder than traditional markets:

- 24/7 trading – no overnight “off” period

- Extreme volatility – double-digit daily moves are normal

- Illiquid altcoins – wide spreads and thin order books increase slippage

A strategy that looks profitable on BTC/USDT may bleed out on a low-liquidity altcoin simply because you can’t get filled at the prices your backtest assumes.

Common Backtesting Traps to Avoid

Even well-intentioned backtests can lie to you. These are the traps that destroy most beginner bot strategies:

1. Overfitting: “Perfect” Backtest, Broken in Real Life

Overfitting happens when you tweak parameters until your backtest looks too good.

- Example: adjusting grid spacing and take-profit levels until a 2021 bull market backtest shows a perfect equity curve with tiny drawdowns.

- Reality: you’ve fitted the strategy to noise in that specific dataset, not to robust market behavior.

A tell-tale sign: extremely high risk-adjusted metrics (e.g., Sharpe > 3) on a small dataset. That’s usually a warning, not a flex.

2. Look-Ahead Bias: Using Future Info in Past Decisions

Look-ahead bias occurs when the backtest uses information that wasn’t actually available at the time a trade would have been made.

Examples:

- Using today’s candle close to decide yesterday’s trade

- Using quarterly data or indicators that require future values

Your backtest then “cheats” without you realizing it.

3. Survivorship Bias: Only Testing Coins that Survived

Survivorship bias means you’re only testing on assets that are still around today, ignoring coins that died or rugged.

- If you backtest a “2020 altcoin strategy” using today’s top 100 coins, you’re only seeing survivors.

- Dead projects (which might have been in your portfolio at the time) are quietly erased from history.

This inflates returns and understates drawdowns. In equities, this bias can add several percentage points to “fake” annual performance; in crypto, with so many dead coins, the distortion can be much worse.

4. Ignoring Fees and Slippage: Death by a Thousand Cuts

Crypto exchanges typically charge 0.1–0.25% per trade.

For a grid bot making 50 trades per week, that’s 5–12.5% of capital churned in fees alone over that period, before considering:

- 0.5–1.5% slippage on liquid pairs

- 1–3% slippage on thin altcoins

A backtest showing +15% annual return can easily drop to 6–8% (or negative) once realistic fees and slippage are applied.

5. Single-Regime Testing: Only Bull Market Data

Backtesting only during a 2021 bull run tells you nothing about:

- How the bot behaves in a 2022-style bear

- How it performs in slow, sideways environments

- What happens during low-liquidity periods

A robust strategy should be at least survivable across multiple regimes, even if it performs better in some than others.

Designing a Simple, Testable Bot Strategy

Complexity doesn’t equal edge. In fact, complex strategies are:

- Harder to backtest properly

- Harder to debug

- Much more prone to overfitting

Start with simple, rule-based systems that are easy to express and measure.

Below are two beginner-friendly templates designed for testability, not magic profits.

Example 1 – Simple Trend-Following Bot (BTC/USDT Spot)

- Market: BTC/USDT spot

- Timeframe: 1-hour candles

Rules:

- Entry: When 50-period EMA crosses above 200-period EMA (golden cross), buy on next candle open.

- Exit: When 50 EMA crosses below 200 EMA, close position on next candle open.

- Stop-loss: Trail stop at 1.5× ATR (Average True Range) below entry price.

- Position size: 2% of total capital per trade.

This type of bot attempts to ride sustained trends while capping downside using volatility-adjusted stops.

Example 2 – Conservative Spot Grid Bot (ETH/USDT)

- Market: ETH/USDT spot

- Grid range: ±5% from current price (upper bound +5%, lower bound -5%)

- Grid lines: 10 evenly spaced levels

- Grid spacing: ~1% per line

- Capital allocation: $500 total, $50 per grid level

- Recenter: Recentre or disable the grid if price breaks outside the range and stays there.

The grid profits by repeatedly buying slightly lower and selling slightly higher inside the defined range. It tends to:

- Excel in sideways, choppy markets

- Underperform or misbehave during strong one-way trends

These are frameworks – not holy grail settings. Their value is that you can write them down clearly, backtest them honestly, and iterate.

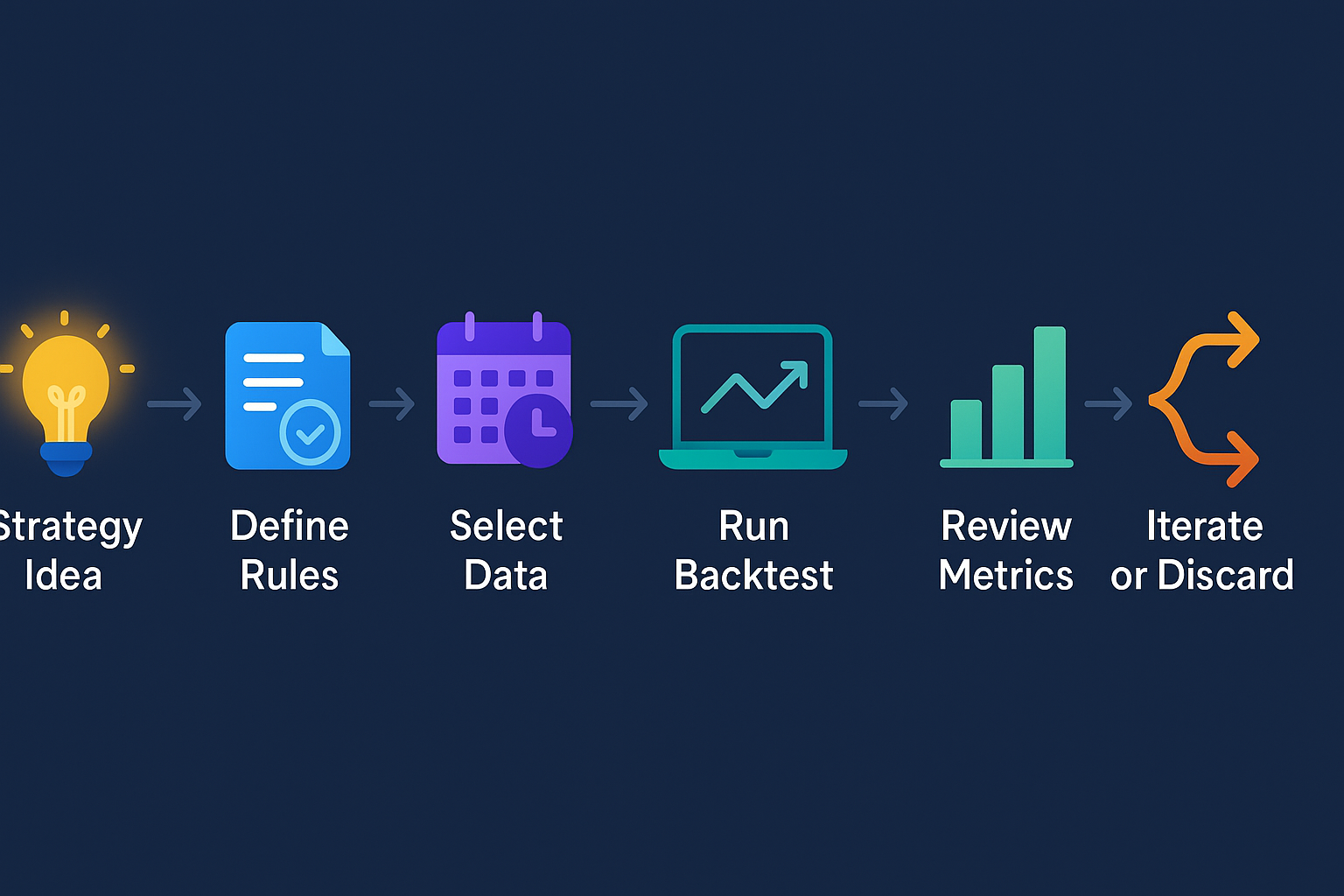

How to Backtest Step-by-Step (Platform-Agnostic)

You can use this workflow on most reputable platforms (TradingView, 3Commas, Cryptohopper, Freqtrade, Backtrader, etc.).

Step 1: Pick Your Asset and Timeframe

For your first backtests:

- Start with BTC or ETH

- Use higher timeframes (1h, 4h, daily)

These markets are more liquid, and higher timeframes reduce noise and false signals.

Step 2: Gather Historical Data

Use at least 1–3 years of data if possible, covering:

- One bull phase

- One bear phase

- Some sideways periods

Most platforms provide built-in OHLCV data from major exchanges.

Step 3: Define Your Rules Clearly

Avoid fuzzy logic like “when it looks bullish”.

Examples of testable rules:

- “Buy when RSI crosses above 40 AND price is above the 200 EMA.”

- “Open a grid from ±5% around current price with 10 levels and no leverage.”

If you can’t write the rule in one clear sentence, it’s probably too complex for a first test.

Step 4: Configure the Backtest

Set:

- Initial capital – e.g. $10,000

- Trading fees – 0.1–0.25% per trade (or whatever your exchange uses)

- Slippage assumptions

- 0.5–1% for BTC/ETH

- 1–3% for altcoins

These assumptions are crucial to avoid overly optimistic results.

Step 5: Run the Backtest

Review:

- The equity curve (PnL over time)

- A trade log (entries/exits, PnL per trade)

- Summary stats dashboard (returns, drawdown, etc.)

Step 6: Evaluate Key Metrics

Pay special attention to:

- Cumulative return – Did it grow capital? By how much?

- Maximum drawdown – Largest peak-to-trough loss.

- Example: $10,000 peak → $7,000 low = -30% drawdown

- Win rate – Percentage of profitable trades.

- A 40–50% win rate can be fine if winners are bigger than losers.

- Risk–reward ratio – Average win ÷ average loss.

- 3:1 is strong; anything >1.5:1 is workable with a reasonable win rate.

- Sharpe ratio – Risk-adjusted performance; >1.0 is acceptable, >2.0 good (be skeptical if >3.0 on small data – could be overfitting).

- Number of trades –

- At least 100–200 trades for intraday systems.

- At least 30–50 trades for swing/position systems.

Small sample sizes are dangerous; you might just be seeing luck.

Step 7: Stress Test by Market Regime

Split your backtest period into segments:

- Bull phases (e.g., Q4 2023)

- Bear phases (e.g., 2022)

- Sideways/choppy phases (e.g., mid-2024)

Ask:

- Does the strategy collapse in any regime?

- Does it behave in line with its design? (E.g., trend bot should suffer in chop but shine in clear trends.)

Step 8: Decide: Iterate or Discard

Set simple rules for yourself, for example:

- If max drawdown > 25–30%, discard or rework.

- If strategy turns flat or negative once realistic fees and slippage are added, discard.

- If performance relies on one very specific period, be suspicious.

Backtesting isn’t about proving your idea is genius. It’s about cheaply discovering where it breaks.

Quick Numeric Example

- Initial capital: $10,000

- Backtest period: 2 years (2022–2024)

- Trades: 120

- Cumulative return: +25% (final balance: $12,500)

- Max drawdown: -18%

- Win rate: 48%

- Average win: $180

- Average loss: $95

- Sharpe ratio: 1.3

This is not “get rich” performance, but:

- Drawdown is under 20% (reasonable for crypto)

- Risk–reward ≈ 1.9:1 (180/95)

- Results are consistent with what you’d expect from a decent trend-following system

This kind of profile is a candidate for paper trading. Not a guarantee – a candidate.

Paper Trading: Bridging the Gap Between Backtest and Live

If backtesting is a flight simulator with last year’s weather, paper trading is flying in today’s weather, but with the plane still on the ground financially.

Paper trading (demo trading, virtual trading) runs your strategy in real time on current market data without using real money.

Many major exchanges and platforms support paper/demo:

- Binance, Bybit, OKX, Kraken, KuCoin (demo/futures testnets or paper modes)

- 3Commas, Cryptohopper, Bitsgap, Gainium, and others via sandbox accounts

Why Paper Trading Matters

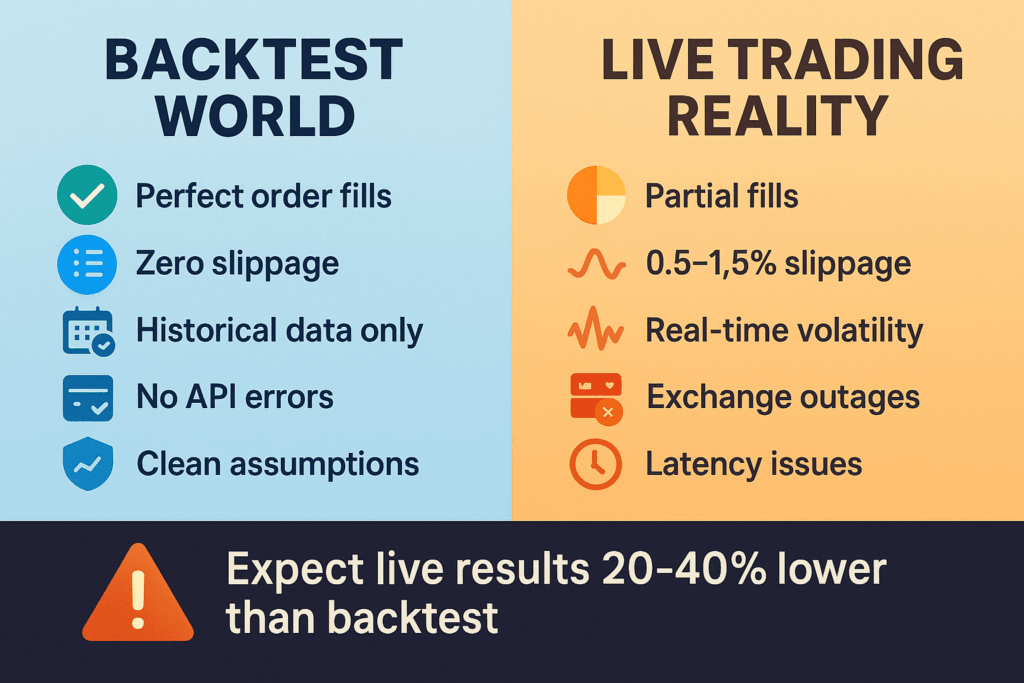

Backtests use clean historical data and idealized order fills. Paper trading exposes your strategy to:

- Current volatility and liquidity conditions

- Exchange outages and API errors

- Real slippage relative to your assumptions

- Latency – orders arriving late during fast moves

In practice, live performance often trails backtest numbers by 20–40% once these frictions are included. Paper trading shows that gap before any real money is at stake.

Step-by-Step Paper Trading Workflow

1. Clone Your Backtested Settings

Take the exact parameters that performed acceptably in backtest:

- Same asset (e.g., BTC/USDT)

- Same timeframe (e.g., 1h)

- Same indicators, grid range, position sizing, and risk rules

Deploy them in a paper account.

2. Keep Asset & Timeframe Consistent

If you backtested BTC 1h, don’t suddenly paper trade SOL 15m.

You want an apples-to-apples comparison between backtest and paper performance.

3. Run Long Enough to Matter

- For intraday strategies: 2–4 weeks minimum

- For slower swing strategies: 4–8+ weeks

The goal is not just to see “a few trades” but to expose the bot to different mini-regimes: small trends, chop, sudden news events, random volatility.

4. Track Metrics Regularly

Daily or weekly, track:

- Daily and cumulative PnL

- Current drawdown

- Win rate

- Number of trades executed

Log these in a simple spreadsheet or Notion doc. Also note qualitative events:

- “Missed one trade during exchange maintenance.”

- “Slippage doubled during CPI news.”

These notes become gold when you review later.

5. Watch How It Handles Real Events

Pay special attention to:

- Fast dumps (e.g., sudden -8% BTC moves)

- Weekends (often lower liquidity)

- Big macro news (Fed decisions, ETF news, exchange issues)

Ask: Did the bot behave like you expected from the backtest? Or did it do something surprisingly dumb?

6. Document Surprises

Write down:

- What aligned with your expectations

- What was worse than expected

- Any technical issues (API errors, missing orders)

- Your own emotional responses (Did you want to interfere? Why?)

This documentation helps refine both your strategy and your mindset.

7. Decide If It’s Ready for Real Capital

Rough rule:

- If paper trading results are within 10–20% of backtest expectations (after fees and slippage) and risk metrics are acceptable → candidate for a small live test.

- If paper results are dramatically worse (e.g., backtest +15%, paper -5%) → pause and diagnose:

- Overfitting?

- Unrealistic backtest fees/slippage?

- Different market regime?

- Bugs in code or configuration?

Don’t move to live until you know what’s going on.

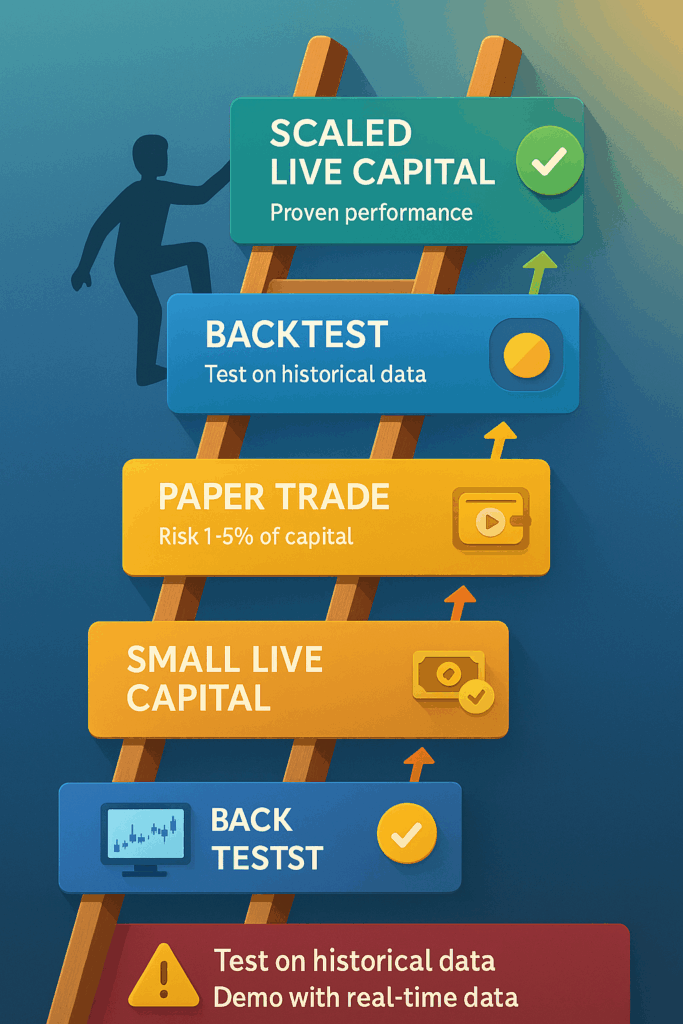

Moving from Paper to Live: How Small Is “Small”?

This is where many traders blow themselves up. A few good paper trades and they throw $5,000 at the bot.

A safer approach:

Start with 1–5% of Your Trading Capital

If you have $10,000 earmarked for bots:

- Start live with $100–$500 on the first strategy.

- Treat it as tuition you can afford to lose while learning.

Use 1x Leverage (Spot Only) for the First Live Test

Your first objective is to test:

- Execution quality

- Bot stability

- Your own ability to stick to the plan

Leverage magnifies both gains and mistakes. Add it later, if ever.

Keep Position Size Tiny

- Risk 1–2% of account per trade on that bot.

- If the bot controls $500, that’s $5–10 risk per trade.

This protects you from catastrophic single-trade failures.

Simple Monitoring Routine

- Daily (5 minutes):

- Is the bot running? Any critical errors?

- Is PnL within expectations? (No surprise -30% days.)

- Weekly (20–30 minutes):

- Compare live performance vs paper vs backtest.

- Review trade logs for strange behavior.

Set Realistic Return Expectations

Because of:

- Slippage

- Fees

- Execution delays

- Missed trades

Live returns are often 20–40% lower than backtest figures.

A healthy mindset:

- Backtest: 10% annual return

- Live expectation: 6–8% would be very good

- Backtest max drawdown: 15% → expect 18–22% live

Judge success by:

- Process adherence

- Whether the bot behaves as designed

—not by whether it matches the perfect backtest curve.

Simple Case Study: BTC Trend-Following Bot

Strategy: 50/200 EMA crossover with 1.5× ATR trailing stop on BTC/USDT 1h.

Backtest (2020–2024, 4 Years)

- Cumulative return: +45%

- Max drawdown: -18%

- Win rate: 48%

- Trades: 87

- Sharpe ratio: 1.4

Result: Modest but solid; acceptable drawdown and risk–reward. Candidate for paper trading.

Paper Trading (4 Weeks, Oct 2024)

- Return: +2.8%

- Max drawdown: -6%

- Win rate: 46%

- Trades: 9

- Notes: 1 missed trade due to API lag; average slippage 0.7% vs 0.5% assumption.

Interpretation: Promising but still a small sample. Behavior aligns with expectations; no major failures.

Live Trading (First 6 Weeks, $500)

- Return: +1.8%

- Max drawdown: -4.2%

- Trades: 11

- Largest losing week: -4% in a choppy range (classic weakness for trend strategies).

Outcome:

- Live returns lower than paper and backtest (as expected).

- Risk stayed within acceptable bounds.

- Strategy behaved as designed.

Decision: Keep running at $500 for a few more months. If performance stays consistent, consider scaling to $1,000.

Mindset: The goal is process validation, not instant wealth. Over 3–6 months of disciplined execution, the trader builds both data and confidence.

Beginner FAQ: Backtesting & Paper Trading

Q1. How many trades do I need in a backtest before trusting it?

For intraday strategies, aim for 100–200+ trades. For swing/position systems, at least 30–50 trades. More important than a raw count is that the backtest spans multiple market regimes (bull, bear, sideways) over at least 1–3 years.

Q2. How long should I paper trade before going live?

Most traders paper trade for 2–8 weeks. High-frequency bots can validate faster (2–4 weeks); slower systems need longer (6–12 weeks) to generate enough trades. Don’t focus on the calendar – focus on whether you’ve seen the strategy handle different conditions and whether the behavior matches your backtest.

Q3. What if my backtest looks great but paper trading is flat or negative?

This is a valuable signal. Common causes:

- Overfitted backtest (tuned to noise)

- Unrealistic assumptions about fees/slippage

- Market regime shift (e.g., you tested a trend bot, but paper trading sits in chop)

- Implementation bugs in your bot

Don’t go live until you understand the gap. Paper losses are cheap tuition.

Q4. Do I need coding skills to backtest?

Not necessarily. Many platforms (3Commas, Cryptohopper, Pionex) offer visual builders and one-click backtesting. TradingView’s Pine Script is beginner-friendly for those who want more control. For maximum flexibility and custom logic, Python frameworks like Freqtrade and Backtrader are powerful—but they’re optional, not mandatory to start.

Q5. Can I use the same strategy on multiple coins after testing it on BTC?

Sometimes, but not automatically. Strategies that work on high-liquidity BTC pairs often suffer on thin altcoins due to higher slippage and erratic volatility. Always paper trade each new asset before risking money. Treat every new coin as a fresh test.

Q6. What is walk-forward analysis, and do I need it as a beginner?

Walk-forward analysis is an advanced technique where you:

- Optimize parameters on one segment of data

- Test them on the next, unseen segment

- Repeat over rolling windows

It’s a strong defense against overfitting. As a beginner, focus first on basic backtesting + paper trading. Once you’re comfortable and want more robustness, explore walk-forward methods.

Conclusion: Test Before You Trade

Backtesting and paper trading won’t make a strategy perfect or guarantee profits. But they dramatically reduce your odds of learning expensive lessons with real money.

Here’s a simple action plan:

- Design one simple strategy (trend-following or conservative grid).

- Backtest it across 1–3 years, including bull, bear, and sideways markets.

- Apply realistic fees and slippage; reject any strategy that only works in perfect conditions.

- If it passes your risk criteria, paper trade it for 4–8 weeks.

- Compare paper results to backtest expectations and document everything.

- If both line up reasonably well, go live with 1–5% of your capital at 1x leverage.

- Monitor closely, have a kill-switch plan, and be ready to pause.

Kill bad strategies with virtual money, not real capital.

When you’re ready to connect this with the rest of the series:

- Revisit “Grid vs DCA Bots: Which Is Better for Beginner Crypto Traders?” if you’re still choosing what to test.

If you stick to this workflow for the next month, you’ll already be far ahead of most people who just copy settings from Twitter and hope for the best.

Discover more from aiCryptoBrief.Com

Subscribe to get the latest posts sent to your email.

")