")

When Bitcoin’s price swings by 20% overnight, stablecoins stay exactly where they’re supposed to be—pegged to $1. This isn’t magic; it’s one of the most ingenious solutions crypto has ever produced. Stablecoins have emerged as the essential glue connecting traditional finance to decentralized ecosystems, enabling everyday transactions, institutional transfers, and complex DeFi operations that would otherwise be impossible in a volatile crypto landscape. By November 2025, the global stablecoin market has surpassed $301 billion in total market capitalization, with over 500 million unique wallet addresses actively using them worldwide. Understanding stablecoins isn’t just important for traders—it’s essential for anyone wanting to grasp how crypto is becoming a genuine bridge to real-world finance.

1. What Are Stablecoins?

Stablecoins are cryptocurrencies designed to maintain a stable value by pegging to external assets, typically a fiat currency like the US dollar. Think of them as the digital equivalent of holding cash in a crypto wallet—you get all the speed and programmability of blockchain technology while preserving purchasing power instead of watching your holdings fluctuate wildly.

The problem stablecoins solve is fundamental to crypto adoption. Bitcoin and Ethereum are revolutionary, but their volatility makes them unsuitable for everyday payments or financial contracts. Imagine you’re a merchant accepting crypto payments. Would you price your products in Bitcoin if your margins could evaporate in hours? This volatility barrier has long prevented cryptocurrencies from functioning as mediums of exchange. Stablecoins eliminate this friction by offering price certainty while retaining blockchain’s advantages: 24/7 trading, minimal fees, instant settlement, and programmable transactions through smart contracts.

Beyond basic transfers, stablecoins serve critical roles in modern DeFi. According to recent data, stablecoins represent over 75% of all DeFi liquidity, powering lending protocols, liquidity pools, and yield-generating platforms where users earn returns on their capital. They enable traders to quickly exit volatile positions without converting to traditional banking rails, institutions to optimize treasury operations across time zones, and DeFi protocols to denominate loans, collateral, and yields in predictable units. In essence, stablecoins are the foundation upon which decentralized finance operates.

2. Why Stablecoins Matter in the Crypto Economy

The importance of stablecoins extends far beyond crypto enthusiasts. Daily stablecoin transactions have doubled in the past 18 months, now facilitating approximately $30 billion in flows globally—still less than 1% of total global money movement, but growing rapidly. This expansion reflects a fundamental shift: institutions and everyday users increasingly view stablecoins as practical infrastructure, not speculative assets.

Stablecoins enable five critical use cases:

- Easy Cross-Exchange Transfers: Traders often move profits to USDC or USDT during market downturns to avoid liquidation. Instead of converting to bank transfers (which take hours to days), they instantly shift stablecoins between exchanges, capturing market opportunities without withdrawal delays.

- DeFi Lending and Borrowing: Protocols like Aave and Compound let users deposit stablecoins to earn interest (typically 3-10% APY in DeFi contexts) or borrow against crypto collateral. This creates a decentralized financial system operating independently of traditional banking.

- Hedging Against Volatility: When crypto markets turn bearish, stablecoins serve as safe harbors. Rather than exiting crypto entirely, users can park funds in stablecoins, earning modest yields while awaiting recovery.

- Cross-Border Payments: Remittance workers and international merchants can now send USDC or USDT instantly across continents for a fraction of traditional wire fees. For emerging markets where traditional banking is expensive or unreliable, stablecoins offer genuine financial inclusion.

- Programmable Treasury Operations: Enterprises can lock stablecoins into smart contracts that automatically execute payments when conditions are met—milestone-based disbursements, syndicated loans, or multi-party settlements—all auditable and compliant by design.

The result is improved liquidity and trust across DeFi ecosystems. Stablecoins provide the certainty that allows complex financial instruments to function. When borrowers know their collateral won’t evaporate due to price swings, and lenders know their returns are denominated in stable units, a functioning credit market becomes possible—one that operates 24/7 without intermediaries.

3. How Stablecoins Work: Three Mechanisms for Maintaining the Peg

Stablecoins maintain their value through three fundamentally different mechanisms. Understanding which mechanism backs a stablecoin is crucial for assessing risk, because each model trades off centralization, efficiency, and resilience differently.

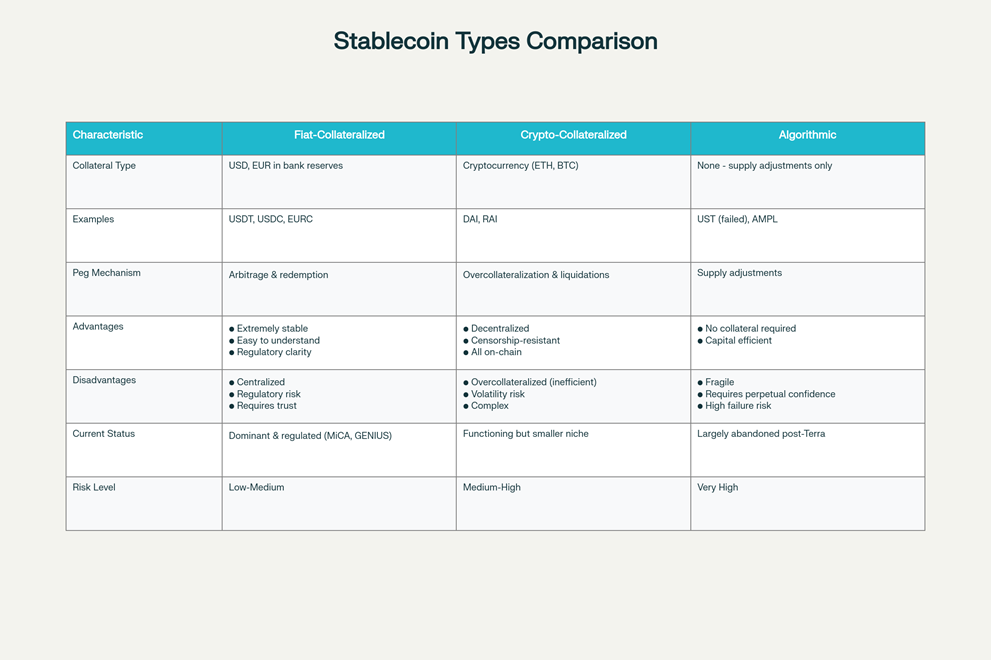

Fiat-Collateralized Stablecoins: Backed by Real Reserves

How They Work: For every stablecoin issued, the issuer holds an equivalent amount of fiat currency (USD, EUR) in bank reserves. When you hold 1 USDT, Tether maintains $1 in reserves somewhere. When you want to redeem, the issuer burns your stablecoin and sends you the underlying fiat.

Examples: USDT (Tether) and USDC (Circle) are the largest fiat-collateralized stablecoins. USDT remains the most widely used, with $176.35 billion in circulation as of October 2025, representing 58% of total stablecoin market share. USDC, with $74.28 billion in circulation, is the second-largest.

How the Peg is Maintained: If USDT trades above $1 on an exchange, arbitrageurs can exploit the difference. They buy USDT at $0.99, redeem it for $1 in cash, pocketing the $0.01 profit. This buying pressure pushes price up. Conversely, if USDT trades below $1, traders can buy $1 worth of fiat, mint new USDT, and sell it for profit, adding selling pressure. This arbitrage mechanism keeps the price anchored to exactly $1.

Advantages:

- Extremely stable because backed by real assets

- Easy for regulators to understand and supervise

- Transparent audit pathways (both USDT and USDC publish reserve attestations)

Disadvantages:

- Centralized: the issuer controls reserves and can freeze accounts

- Regulatory risk: governments can pressure issuers or restrict banking relationships

- Requires trust in custodians holding reserves

Reserve Composition in 2025: Tether holds approximately $98.5 billion in U.S. Treasury bills, making it one of the largest non-sovereign holders of government debt globally. USDC maintains segregated reserves across regulated banks and short-term Treasury instruments.

Crypto-Collateralized Stablecoins: Backed by Other Cryptocurrencies

How They Work: Users lock crypto (usually Ethereum) into a smart contract to mint a stablecoin. Critically, these systems are overcollateralized—you might deposit $150 worth of ETH to mint only $100 of stablecoin. This excess collateral acts as a buffer against price drops.

Example: DAI (MakerDAO) is the most successful crypto-collateralized stablecoin, with approximately $3.78 billion in circulation. It’s maintained via a decentralized protocol where governance token holders manage the system.

How the Peg is Maintained: If DAI’s price rises above $1, holders are incentivized to mint more DAI (increasing supply and pushing price down). If it falls below $1, the protocol automatically liquidates undercollateralized positions, removing supply and pushing price back up. The smart contract maintains these mechanics autonomously.

Advantages:

- Fully decentralized—no central issuer can freeze your funds

- All collateral and transactions visible on-chain

- Censorship-resistant by design

Disadvantages:

- Volatility risk: collateral (ETH, BTC) can lose value quickly, forcing liquidations

- Overcollateralization inefficiency: ties up significantly more capital than fiat-backed models

- Complexity: requires understanding of liquidation mechanisms and oracle risks

Algorithmic Stablecoins: Pegged Through Code Alone

How They Work: No collateral required. Instead, algorithms automatically adjust token supply based on price deviations. If the stablecoin trades above $1, the algorithm mints new tokens (increasing supply, pushing price down). If it trades below $1, tokens are burned (reducing supply, pushing price up).

The Case Study: Terra’s UST Collapse (May 2022): UST attempted to maintain its peg through an algorithmic relationship with LUNA, its companion token. Whenever UST traded below $1, holders could burn 1 UST to mint $1 worth of LUNA, theoretically guaranteeing redemption. The system also offered an unsustainable 20% annual yield through the Anchor protocol, attracting massive inflows.

When confidence eroded (triggered by a $85 million trade on Curve Finance), UST holders rushed to exit. The system minted trillions of new LUNA tokens to satisfy redemptions, flooding the market and collapsing LUNA’s price from $116 to near zero. This “death spiral” wiped out nearly $40 billion in value and shattered confidence in algorithmic stablecoins. Today, algorithmic stablecoins without collateral backing are effectively banned under the EU’s MiCA regulation.

Lesson Learned: Algorithmic peg mechanisms are fundamentally fragile. They depend on perpetual market confidence and circular logic (two assets backing each other). Without collateral reserves, no floor exists to stop the collapse. Most modern stablecoin projects have abandoned this model in favor of collateralization.

4. The Most Popular Stablecoins in 2025

The stablecoin landscape in 2025 is dominated by three categories: established fiat-backed giants, emerging crypto-backed alternatives, and commodity-backed tokens. Here’s what’s actually being used:

USDT (Tether) — The Market Leader

Market Position: $176.35 billion in circulation (58% market share). USDT is the oldest stablecoin (launched 2014) and the most widely supported across exchanges, blockchains, and DeFi protocols.

How It Works: Fiat-collateralized on the Tether platform. Quarterly attestations from accounting firm BDO confirm reserves.

Key Update for 2025: In March 2025, Tether announced it is “engaging with a Big Four accounting firm” (PwC, EY, Deloitte, or KPMG) to conduct the first comprehensive audit of its reserves—a significant shift toward full transparency. Previously, Tether relied on quarterly attestations. Ardoino, Tether’s CEO, indicated this is now “the highest priority” and the pro-crypto Trump administration has made it more feasible.

Reserves Breakdown: Approximately $98.5 billion in U.S. Treasury bills (as of Q1 2025), with 99% managed by Wall Street brokerage Cantor Fitzgerald. Remaining reserves held as cash and cash equivalents.

Why It Dominates: Ubiquitous availability, high liquidity, and network effects. If you’re trading on a smaller exchange, USDT is almost certainly available.

USDC (Circle) — The Transparent Challenger

Market Position: $74.28 billion in circulation (24.3% market share). USDC is regulated, transparent, and increasingly favored by institutions and compliant platforms.

How It Works: Fiat-collateralized, with Circle maintaining segregated reserves at BNY Mellon and other custodians. USDC was the first stablecoin to obtain a license under the EU’s MiCA regulation.

Key Update for 2025: Circle is now publicly traded (post-IPO in mid-2025), increasing its regulatory obligations and disclosures. In Q2 2025, Circle reported $658 million in reserve income—a 50-53% year-over-year increase—reflecting massive expansion in USDC circulation, which hit $61 billion on average in Q2 2025, up approximately 90% year-over-year.

Why It’s Growing: Institutions prefer USDC’s transparency. It’s also the primary stablecoin on Base (Coinbase’s Ethereum scaling layer), making it essential for institutional DeFi.

DAI (MakerDAO) — The Decentralized Option

Market Position: $3.78 billion in circulation. Though much smaller than USDT or USDC, DAI represents the most sophisticated crypto-collateralized model.

How It Works: Users deposit Ethereum (ETH), Staked Ether (stETH), and other assets as collateral to mint DAI. The system is governed by MKR token holders, who vote on collateral types, stability fees, and protocol upgrades.

Why It Matters: DAI demonstrates that decentralization is possible without sacrificing stability. It’s used extensively in DeFi for lending, yield generation, and complex financial instruments. It’s also the only major decentralized stablecoin that has never lost its peg (unlike numerous failed algorithmic competitors).

Emerging Alternatives

USDe (Ethena): $7.56 billion in circulation. Backed by short positions in perpetual futures, offering a novel collateralization mechanism.

FRAX: $299.51 million in circulation. A hybrid model combining fractional fiat collateral with algorithmic supply adjustments.

Commodity-Backed Options:

- Tether Gold (XAUt): $823.7 million, backed by physical gold held in Swiss vaults

- PAX Gold (PAXG): $940.67 million, also gold-backed

- EURC: $209.29 million, pegged to the Euro

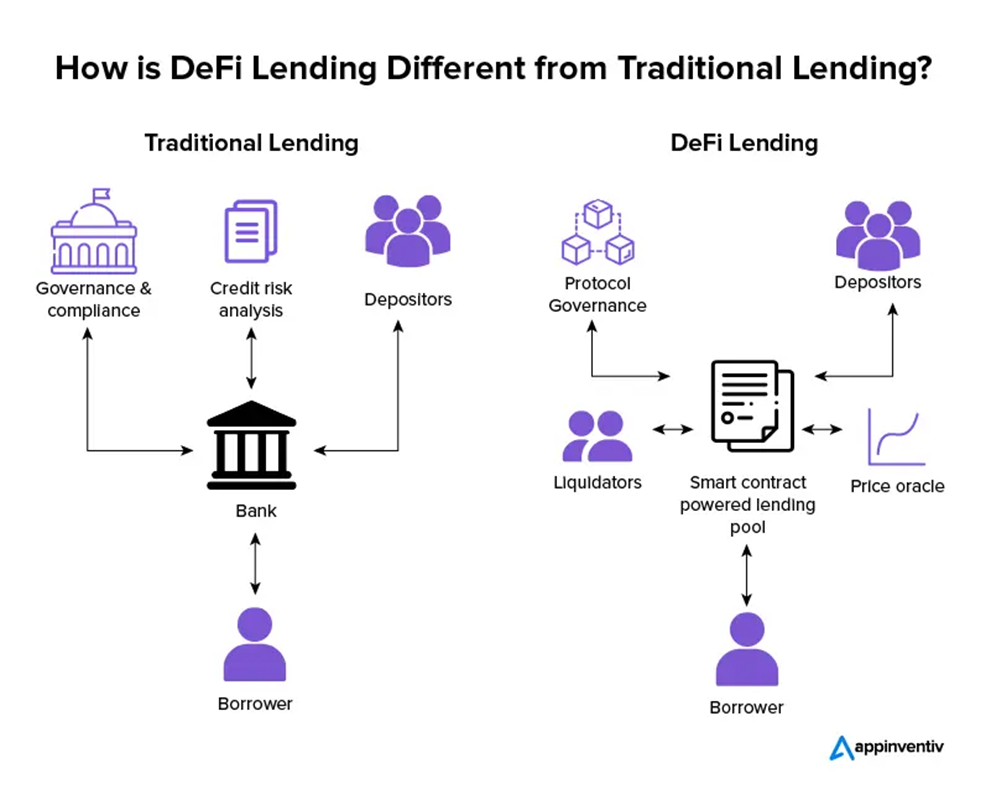

5. The Role of Stablecoins in DeFi: The Foundation of Decentralized Finance

Stablecoins aren’t just a feature of DeFi—they’re its foundation. Without them, decentralized finance would be impossible. Here’s why:

Enabling Lending and Borrowing

DeFi lending protocols like Aave, Compound, and Curve allow users to deposit stablecoins and earn interest. Typical yields range from 3-10% APY depending on borrowing demand, market conditions, and whether the platform is offering incentives. This is attractive compared to traditional savings accounts (which offer <0.5% APY in many regions).

The mechanics work like this: Borrowers post crypto collateral (usually valued at 150%+ of the loan) and borrow stablecoins. They pay interest to lenders. Lenders supply stablecoins and earn that interest. All of this happens automatically through smart contracts, 24/7, without banks or intermediaries.

Liquidity Pools and Yield Farming

Stablecoins represent over 75% of all DeFi liquidity, according to DeFiLlama data. This means the vast majority of trades between different crypto assets flow through stablecoin pairs. USDC/ETH, DAI/USDT, and similar pairs are the most liquid markets, enabling efficient price discovery and minimal slippage.

Users can deposit stablecoin-to-stablecoin pairs (e.g., USDC+USDT) into liquidity pools and earn fees from traders. Some platforms also offer governance token incentives, creating temporary yields exceeding 12% APY during launch periods.

Enabling Complex DeFi Products

Once stablecoins provide a stable unit of account, DeFi developers can build more sophisticated instruments:

- Lending Pools: Institutions can syndicate loans using smart contracts, with repayments managed automatically

- Structured Products: Programmable disbursements triggered by market conditions (e.g., “pay $1M if ETH breaks $2,000”)

- Capital Markets: Tokenized stocks and bonds can be issued 24/7 and settled on-chain in stablecoins

Learn more in our What is DeFi? A Comprehensive Guide to Decentralized Finance pillar page—the foundation of decentralized finance.

6. Risks and Challenges: What Can Go Wrong

While stablecoins are revolutionary, they’re not risk-free. Understanding these challenges is critical for anyone using them.

Reserve and Transparency Risk

Fiat-backed stablecoins depend entirely on the issuer maintaining claimed reserves. If Tether really held $1 in reserves for every USDT in circulation, it’s safe. If not, it’s essentially a fractional reserve scheme. This trust dependency is why Tether’s lack of a full audit (until recently) remained controversial.

Pro Tip: Always check whether a stablecoin’s reserves are independently audited. USDC publishes detailed reserve attestations and is subject to New York banking regulations. USDT is moving toward full Big Four audits in 2025. Stablecoins with no audit history or vague reserve claims are much riskier.

Smart Contract Risk for Crypto-Collateralized Coins

Crypto-backed stablecoins like DAI rely on smart contracts to manage overcollateralization, liquidations, and price feeds. Any vulnerability in these contracts can be exploited. Recent DeFi exploits have demonstrated this danger:

- Euler Finance (March 2023): $197 million in losses, including significant stablecoin drains, due to smart contract vulnerabilities

- Curve Finance (July 2023): Hundreds of millions in stablecoin liquidity put at risk due to protocol exploits

These attacks illustrate how stablecoin security is intertwined with DeFi protocol security. A single contract bug can cascade through multiple platforms.

Regulatory Uncertainty

In 2025, stablecoin regulation is rapidly crystallizing, creating both clarity and risk:

EU’s MiCA (Market in Crypto-Assets Regulation): Fully in effect since January 2025, MiCA requires stablecoin issuers to maintain 1:1 liquid reserves and obtain Electronic Money Institution (EMI) licenses. Non-compliant stablecoins have been delisted by major exchanges (Kraken delisted USDT, PYUSD, and others by March 31, 2025).

U.S. GENIUS Act (Passed July 2025): Establishes a federal framework requiring payment stablecoin issuers to hold 100% audited reserves in cash or short-term Treasuries, publish monthly disclosures, and provide redemption rights at par.

The Risk: Regulatory changes can restrict access. In Europe, non-compliant issuers face delistings. In the U.S., stablecoins that fail to comply with GENIUS requirements could face criminal penalties and market restrictions.

Algorithmic Stablecoin Failures

The Terra UST collapse remains the cautionary tale. Algorithmic stablecoins proved fundamentally flawed because they lack collateral reserves to support redemptions during crises. When confidence erodes, no floor exists to prevent total collapse.

Notably, the first week of November 2025 saw three major DeFi stablecoins lose their pegs simultaneously, including notable protocols that had survived previous crises. These recent failures underscore that decentralized stablecoins remain vulnerable to liquidity crises and smart contract exploits.

Depeg Events and Liquidity Crises

Even well-designed stablecoins can temporarily lose their peg during market stress. Liquidity crises occur when too many holders attempt to redeem simultaneously, depleting liquidity pools. Automated market makers (AMMs) then sell collateral at reduced prices, pushing prices further down.

Three Failure Modes:

- Liquidity Crises: Redemption requests exceed available liquidity in pools

- Collateral Shock: Backing assets (ETH, BTC) lose value rapidly, reducing collateral ratios below safety thresholds

- Smart Contract Failures: Bugs or oracle failures cause unintended liquidations or supply changes

7. The Future of Stablecoins: 2025 and Beyond

The stablecoin landscape is evolving rapidly. Here are the trends shaping 2025 and beyond:

Real-World Asset (RWA) Integration

Stablecoins are increasingly backing more than fiat currency. Some issuers now include tokenized real-world assets—Treasury bonds, commercial paper, mortgage-backed securities, and even physical commodities—in reserve portfolios. This diversifies backing while offering higher yields to reserve holders.

Circle’s USDC reserves include short-term Treasury instruments, which earn interest that Circle reinvests into the protocol (contributing to that 50-53% YoY increase in reserve income mentioned earlier).

Stablecoin Regulation and Transparency

Both MiCA and the GENIUS Act represent a regulatory consensus: transparent, fiat-backed stablecoins with strong prudential safeguards are the future. This is good news for USDC and USDT, which already meet or exceed most requirements. It’s bad news for projects lacking reserves or clear governance.

The enforcement of these frameworks is already reshaping the market. In Europe, exchanges have delisted non-compliant tokens. In the U.S., the GENIUS Act provides a path for legitimate stablecoin issuers while creating barriers for unregistered competitors.

Multi-Blockchain Expansion

USDC has been deliberately expanding across blockchains: Ethereum, Solana, Polygon, Arbitrum, Optimism, Base, and many others. This multi-chain strategy increases utility and reach while reducing any single blockchain’s operational risk.

Tether similarly maintains USDT across numerous chains, though it began with Ethereum and expanded slowly.

CBDCs and the Competition

Central banks are developing their own digital currencies (CBDCs)—government-issued digital money. The European Central Bank, People’s Bank of China, and others are investing heavily in CBDCs.

Interestingly, research shows pro-CBDC rhetoric from central banks reduces stablecoin supply as markets anticipate future regulatory pressure or displacement. However, CBDCs and stablecoins likely serve different niches:

- CBDCs: Better for government control, monetary policy, and domestic payments

- Stablecoins: Better for DeFi, cross-border payments, programmability, and 24/7 settlement

The Trump administration has signaled support for private digital money (stablecoins) alongside CBDCs, suggesting coexistence rather than replacement in the U.S.

Final Thoughts

Stablecoins have evolved from experimental curiosities to essential infrastructure bridging traditional finance and decentralized ecosystems. By November 2025, the $301 billion stablecoin market demonstrates their essential role in global crypto adoption. USDT and USDC enable trillions in DeFi value, cross-border payments, and institutional-grade financial operations that simply weren’t possible five years ago.

Yet risks remain. Reserve transparency, regulatory changes, and DeFi vulnerabilities can all affect stablecoin stability. The lesson from Terra’s collapse and recent DeFi exploits is clear: not all stability mechanisms are equal. Fiat-backed, collateralized models with transparent reserves have proven robust, while algorithmic-only approaches are too fragile for financial infrastructure.

As you explore stablecoins, prioritize projects with:

- Independent reserve audits or attestations

- Regulatory compliance (MiCA in EU, GENIUS-ready in U.S.)

- Transparent governance and reserve composition

- Multi-blockchain support for redundancy

The future of stablecoins is bright, but it belongs to transparent, well-capitalized, regulated issuers—not to speculative experiments promising unachievable yields.

Discover more from aiCryptoBrief.Com

Subscribe to get the latest posts sent to your email.